THE stocks managed to maintain their shine in the sixth eventful week as investors were not inclined to miss the rising market ensuring massive capital gains during each session.

THE stocks managed to maintain their shine in the sixth eventful week as investors were not inclined to miss the rising market ensuring massive capital gains during each session.

Announcement of impressive cash dividend plus bonus shares by some leading banks did not allow the investors to sit on the sidelines even for a day and what it would be once the payouts dried was still unclear. But some analysts predicted a shakeout of about 200 points in the index once the current buying euphoria fades out.

Along with oil giants, the National Bank remained the star performer and settled well above the widely speculated level of Rs300 and so did some other leading banks, including the MCB and the Bank of Punjab despite the post-dividend selling.

The market passed through a mid-week mild interruption on technical selling but the stocks maintained their bullish outlook boosted by fresh heavy buying in oil and bank shares amid reports of higher dividend and privatization of some oil giants, including the PSO possibly during the current year.

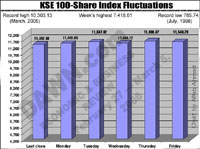

The chief positive factor behind the virtual run-on in oil shares were the reports of new oil and gas finds in the NWFP province. However, the size of the reserves was yet to be determined but it was said to be there and could significantly add to the existing deposits. The KSE 100-share index broke through three barriers at 11,600 points, adding Rs71 billion to the market capital at Rs3,287.00 billion.

Leading oil giants, notably the OGDC, the Pakistan Petroleum, and the Pakistan Oilfields which have big stakes virtually raced toward their new chart points finishing with limited gains.

The National Bank led the run-up in the banking sector on reports that it will sell its stakes to the Saudi Al-Jazeera Bank thus adding to its earnings. It briefly touched the high market of Rs300 against the face value of Rs10. Others, notably the Faysal Bank, the MCB and the Bank of Punjab followed them amid reports of higher payouts.

Analysts said that the current run-up was expected to remain sustained in coming weeks also, as board meetings of many leading companies were due during the next couple of sessions and there was a strong possibility of higher interim payouts by the bank, and cement shares.

The other aiding factor was smooth rolling over of outstanding positions from the matured February contracts to the ruling March despite fears of some problems. This gave a free-hand to punters and speculators to indulge in renewed buying.

The market may be looking beyond the index level of 12,000 points as the developing situation on the bank and oil sectors suggests, said leading analysts but some others said that there could be pruning on the overvalued counters before the renewed run-up.

The market’s buoyant mood despite negative press comments on the current price flare-up was well-reflected in the KSE 100-share index which was heading towards its next target of 12,000 points on the strength of higher corporate earnings and steadily increasing foreign support on the selected counters.

Click to view the larger image

After having touched at one point the week’s highest at 11,657.36 points, it finally ended with fresh gain as compared to previous 11,546.79 points, showing a gain of 194 points.

All leading current favourites finished with the limited gains at their career-best levels as investors were not inclined to take an overview of their being terribly overvalued and fraught with high risks despite talks of higher cash dividend and bonus shares.

Earlier, it was higher by 140 points but the weakness of the OGDC halted its upward drive. Massive buying in the PTCL, the National Bank, the MCB, the D.G. Khan Cement and the PSO did not allow it to show sign that the current run-up was overdone.

Opinions were, however, divided over the market’s future trend being in a highly overbought position. Some said that it could take a breather after having touched the index level of 12,000 points on the strength of overdue corporate announcements, notably from the banking and cement sectors.

The current week was a rollover week as investors will have to square their outstanding position for the February future contracts, some analysts said adding that as positions in some of the leading scrips were quite high there could be selling in them followed by sympathetic unloading in others.

However, much will depend on the intensity of the sell-off and the market’s absorption capacity they said adding that if there were rollover problems it might follow panic selling.

But some others said that the technical reaction may be as aggressive as speculated by some brokers because the ground realities signal that both leading local and foreign buyers may not be deterred by any amount of sell-off on technical grounds.

Leading gainers were led by the Sanofi Aventis, the United Bank, the Attock Petroleum, the Mari Gas, the Pakistan Oilfields, the Pakistan Petroleum, the OGDC, the Ferozesons Lab, the Nestle Pakistan, the Rafhan Maize, the Millat Tractors followed by the National Bank and the MCB. The losers included Bhanero Textiles and many others.

Prominent losers included the Wyeth Pakistan, the Treet Corporation, the Colgate Pakistan, Thal, the Atlas Honda, the Arif Habib Securities, the PSO, the Gillette Pakistan, the IGI, and the Lakson Tobacco.

FORWARD COUNTER: Speculative issues on the forward counter followed the lead of their counterparts in the ready section and generally finished higher under the lead of oil, bank and fertilizers shares. The IT sector also performed credibly well followed by the reports of higher earnings and good payouts by some.

The National Bank, the OGDC, the Pakistan Petroleum, the Pakistan Oilfields, and some cement and leading shares on other counters also rose amid active trading.—Muhammad Aslam